By Jon Styf, The Center Square, Aug 25, 2021 – Tennessee has disbursed only $17.2 million of the

Nearly $2 million of the amount has been paid out in the past two weeks, but it still pales in comparison to the total money available, with $312 million more applied for and received from the state in Phase 2 of the program, called ERA2.

The Tennessee Housing Development Agency distributes the rental relief in 91 of Tennessee’s 95 counties, while some larger counties, such as Davidson and Shelby counties, distribute the funds through their own local agencies.

“In Tennessee and many other states, the number of applications for COVID rent relief are far fewer than expected,” THDA spokesperson Rebecca Anderson said. “THDA is continuing outreach efforts to landlords, tenant groups, social service agencies and non-profits. THDA is also working with the Administrative Office of the Courts to make those who are facing eviction aware of the program.”

Only 12% of the federal rental assistance funds had been distributed nationwide as of June 30. Only five states had distributed more than 20% of their funds, and only 10% of localities distributed more than 50%. Tennessee ranked 31st in the nation in the amount of funds distributed through the end of June.

To combat the low fund distribution rates, the Biden administration has continued to ask states to do what they can to simplify and speed up the process of fund distribution.

“For months, the administration has worked to speed up state and local grantees’ delivery of ERA and help keep American families stably housed,” the White House said Wednesday in a news release. “As the president has made clear, no state or locality should delay distributing resources that have been provided by Congress to meet families’ critical needs and prevent the tragedy of unnecessary eviction.

“Most notably, today, Treasury is providing even more explicit permission for grantees to utilize self-attestation without further documentation in order to speed the delivery of assistance to households in need during the public health emergency.”

The lack of fund distribution also directly impacts landlords.

Gary Heath, president of Good Landlords in Louisville, Tennessee, said no landlord wants to have to evict a tenant who cannot pay rent.

“It is usually a last resort to resolve an undesired situation. It’s expensive and time-consuming and leaves a landlord with an empty unit to repair and restore,” Heath said. “Many landlords are small operations with only a few units. When a tenant or two doesn’t pay their rent as expected, it may put the owner in a dire condition. They have mortgages to pay, taxes and insurance and other cost any property owner has to deal with. Any homeowner with a mortgage who suddenly loses their income would probably struggle with the same emotions many landlords feel today.

“I understand politicians and uninvolved citizens wanting to protect tenants who are truly having a hard-time at no fault of their own, but I wish they wouldn’t ignore how their decisions affect a struggling property-owner.”

Heath said he has referred a few tenants to the rental relief program but several have struggled to acquire payments.

“Sadly, some of the people who need the help don’t have access to the internet, a few don’t even have an email address,” Heath said. “When they called the number, they were told they’d have to apply on line. Online is still unknown territory to many uninformed individuals who need the help.”

The THDA's Anderson encouraged those who are struggling to receive benefits to call the THDA Rent Relief call center at 844-500-1112.

The White House said it is encouraged that July’s distribution numbers look better than previous months. In July, 341,000 households received rental and utilities assistance, up from 293,000 in June and 157,000 in May, the White House said.

Anderson said the TDHA is looking continuously for ways to increase its distributions.

“To name just a few improvements made, THDA has decreased the amount of uploaded documentation required by an applicant and simplified the process for obtaining prospective rent payments for eligible applicants,” Anderson said. “We will continue to monitor and evaluate the program and make adjustments, when appropriate, to help better serve Tennesseans in need of this funding.”

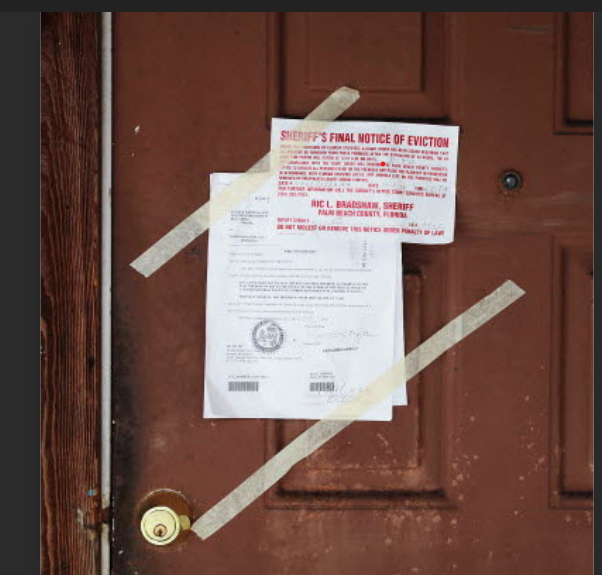

A nationwide eviction moratorium ended at the end of July, but the Centers for Disease Control and Prevention extended the moratorium shortly after it ended. However, a ruling from the 6th U.S. Circuit Court of Appeals determined the moratorium did not apply in Tennessee and the surrounding states that it serves.

“Has the eviction moratorium affected me and other landlords in the state? Of course, it has,” Heath said. “When a tenant doesn’t pay their rent, it disrupts the chain of commerce. It could cause a ripple that affects banks and suppliers. It puts the entire burden of supporting these tenants in the laps of the landlords.”

Top Stories